Over the last year, student loan programs have changed dramatically. SAVE is going away. The RAP plan is taking its place. And the caps on federal borrowing will have ripple effects across the medical community. It’s natural to have a sense of uneasiness and stress as you look toward the future of navigating your student loans.

You are busy and work in a profession that can feel extremely gratifying and exhausting at the same time. Carving out spare time to research federal student loan policy (134 pages full of legalese) is not an enjoyable endeavor. Especially when it seems to change so often.

In this post, I’ll discuss what you need to know about RAP and the student loan program changes going into effect on July 1, 2026.

What Happens to Those Currently in the SAVE Program?

After a two-year legal battle, the Saving On A Valuable Education (SAVE) program is officially coming to a close. When SAVE launched in late 2023, it was widely considered the best Income Driven Repayment (IDR) option available. That’s no longer the case.

Borrowers in SAVE benefited from an interest subsidy and payment pause from the summer of 2024 to the summer of 2025, similar to the COVID pause. However, interest resumed in August 2025, and the forbearance time in SAVE is not initially considered eligible as credit for any federal forgiveness program. If you are pursuing Public Service Loan Forgiveness (PSLF) or IDR forgiveness, those ~two years may not count toward your total. There is a potential remedy to the SAVE forbearance—the PSLF buyback program—but it has been largely stalled by the Department of Education, with processing times currently exceeding three years.

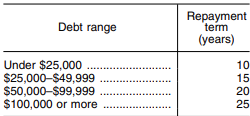

On July 1, 2026, borrowers in SAVE will have 90 days to select a new repayment plan. If no plan is selected, you’ll automatically be moved to standard repayment or the newly created tiered standard repayment plan. Tiered standard repayment is the new default payment program for federal loan borrowers who borrow later than June 30, 2026. Payment terms are based on how much you owe.

For most white coat investors, the repayment term would be over 25 years. This payment program does not qualify for the PSLF program.

More information here:

Helping a Pre-Med Run the Numbers on Medical School

What IDR Plans Are Available Now?

Income Driven Repayment (IDR) plans are changing because of the OBBBA bill passed in 2025. Currently, a borrower can enroll in:

- Old Income Based Repayment (IBR): 15% of discretionary income for those who borrowed pre-July 1, 2014

- New Income Based Repayment (IBR): 10% of discretionary income for those who borrowed post-July 1, 2014

- Pay As You Earn (PAYE): 10% of discretionary income

- Income Contingent Repayment (ICR): 20% of discretionary income

The newest IDR plan, called the Repayment Assistance Plan (RAP), is expected to be available in July 2026.

All of these plans qualify for PSLF. However, ICR and PAYE will sunset by July 2028. Borrowers need to be thinking ahead about which plan works best for their student loan plan.

What Is the Repayment Assistance Plan (RAP)?

Repayment Assistance Plan or RAP is the newest iteration of IDR plans created by OBBBA. RAP has features that are like the SAVE/REPAYE plans, where it subsidizes all unpaid interest. This ensures that if you make your required payment, your loan balance will never go higher.

For example, if your interest grows $1,000 per month and your required payment in RAP is $300, the unpaid interest of $700 is waived ($1,000-$300 = $700). The interest subsidy can be very helpful to those who are in early career or in training. Typically, the subsidy phases out as income increases when you move into practice.

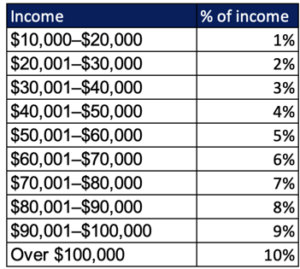

Payments in RAP are calculated as a percentage of Adjusted Gross Income.

If your income is below $10,000, the minimum payment is $10 per month and $120 for the year. Unlike legacy IDR plans, RAP does not use a federal poverty line deduction. Instead, it deducts $50 per month per child (two kids = $100 per month off your payment).

RAP has no payment ceiling, requires direct federal student loans, qualifies for PSLF and includes a private sector forgiveness track at 30 years (longer than previous IDRs). Married borrowers can file taxes separately to exclude spousal income. One distinct feature is that payments made while on RAP do not count toward private sector forgiveness eligibility under any other Income-Driven Repayment (IDR) plans.

Here are a few examples of monthly payments:

- Single resident earning $60,000 per year: ($60,000 / 12 * 5%) = $250 per month

- Single resident earning $60,001 per year: ($60,001 / 12 * 6%) = $300 per month

Please note: the RAP plan includes a sharp payment cliff, where even a small increase in AGI can significantly raise your monthly payment. Reducing your AGI by just a few dollars may help lower your required payment and increase your savings.

- Single attending earning $375,000: ($375,000 / 12 * 10%) = $3,125 per month

- Married attending earning $375,000 with three kids: ($375,000 / 12 * 10%) – 150 = $2,975 per month (note the lower monthly payment due to the household's three children)

Is RAP the Right Plan for Me?

RAP is an IDR plan that you can utilize to progress toward PSLF or private sector forgiveness, and it is the only IDR plan option if you take a loan out later than June 30, 2026. RAP stacks up well against Old IBR and ICR. However, it appears to be more expensive than New IBR and PAYE.

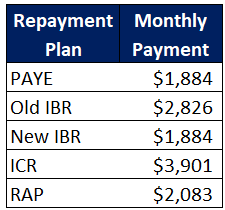

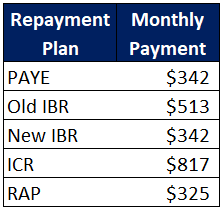

Scenario #1 — High Debt Relative to Income

Single physician, $400,000 of student loans, pediatrics, earning $250,000.

RAP is well below Old IBR and ICR but slightly higher than PAYE and New IBR. Let’s now lower the debt balance for this physician.

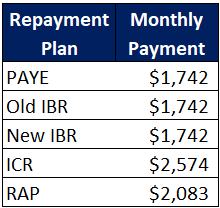

Scenario #2 — Lower Debt Relative to Income

Same physician earning $250,000, $150,000 of student loans.

RAP’s payment doesn’t change. But you’ll notice PAYE and the IBRs are all lower due to the payment cap that kicks in when income starts to exceed the loan balance. The payment cap is a relevant factor for your student loan plan if you are considering PSLF and if you'll earn income higher than your student loan balance.

Scenario #3 — Trainee

Trainee earning $65,000 with $150,000 of student loans.

At lower incomes, most plans (other than ICR) land in a similar range. The key differentiator is RAP’s interest subsidy, which can keep your loan balance from growing.

Choosing the right repayment plan is an important step in successfully managing your student loans and staying aligned with your financial goals. If you’d like help determining which repayment strategy is best for your situation, schedule a time to meet with Student Loan Advice today.

More information here:

Need Private Student Loans? We Can Help!

Critical Student Loan Deadlines Before July 1, 2026

Here are the most time-sensitive changes that could impact your student loan plan right now.

Any New Federal Loan Issued on July 1, 2026, or Later

This is the most underappreciated change in the legislation. If you take out any federal loans on or after July 1, 2026—even a small one—you become ineligible for all IDR plans except RAP.

This applies to federal consolidation loans as well. A direct federal consolidation typically takes 4-8 weeks to process, and the loan date is determined by disbursement, not application. If you're considering a federal direct consolidation right now, there's a meaningful chance your loan won't disburse until July 1 or later, running the risk of permanently closing off IBR and PAYE as options.

New Federal Borrowing Caps

New federal borrowing caps students starting their program of study after June 2026. Previously, a professional or graduate student could federally borrow up to the cost of attendance with the advent of Grad PLUS loans. With Grad PLUS loans discontinued, federal borrowing caps will be:

- $200,000 ($50,000 per year) for medical and dental school

- $100,000 ($20,500 per year) for graduate school

- $257,500 lifetime cap across all federal borrowing

For students in the class of 2030 and beyond, private borrowing will become much more common to cover the funding gap. Programs like PSLF will be less generous with fewer IDR options and lower federal balances owed.

If you need private student loans, WCI can help. We've partnered with several great companies that can provide great service and fair terms (plus, you'll get cash back and a free WCI course).

† Bonus may include cash rebates and value of free course. Student loan borrowers who use the WCI links will be enrolled in The White Coat Investor’s flagship course, Fire Your Financial Advisor: STUDENT for free ($99 value). Borrowers may still receive the amazing cash rebates that WCI has negotiated with lenders. Offer valid for loan applications submitted from May 1, 2026 through October 31, 2026. Free course must be claimed within 90 days of first loan disbursement. To claim free course enrollment, visit https://www.whitecoatinvestor.com/loanbonus.

For new private student loans, we recommend you check with two or three of these companies and go with the one offering you the lowest interest rate and best terms.

What Should You Do Right Now?

The window for some of you to act is narrow.

- If you’re a PSLF candidate still on SAVE, start comparing IBR, PAYE, and RAP now, as you need to act soon.

- If you're in SAVE and not pursuing forgiveness, consider privately refinancing your student loans.

- If you're planning to consolidate now, understand that your new loan will almost certainly disburse on or after July 1, locking you into RAP.

Everyone's situation is different. Running your own numbers that factor in income, family situation, loan balance, and employment goals is the only way to know which path is best for you. If you'd like help working through it, the team at Student Loan Advice can walk you through the specifics.

What do you think? Are you planning on enrolling in RAP? Are you still in SAVE forbearance? Why or why not?