Medical practice in 2026 looks drastically different from what it did a decade ago. There was a time when malpractice exposure felt more predictable and short-lived. That is no longer the case. Larger jury awards, longer filing windows, delayed discovery of injuries, and litigation funding are driving verdicts beyond traditional policy limits.

At the same time, patients are often presenting later and sicker, creating missed opportunities for earlier intervention and increasing the likelihood of poor outcomes—even when earlier access was outside a physician’s control.

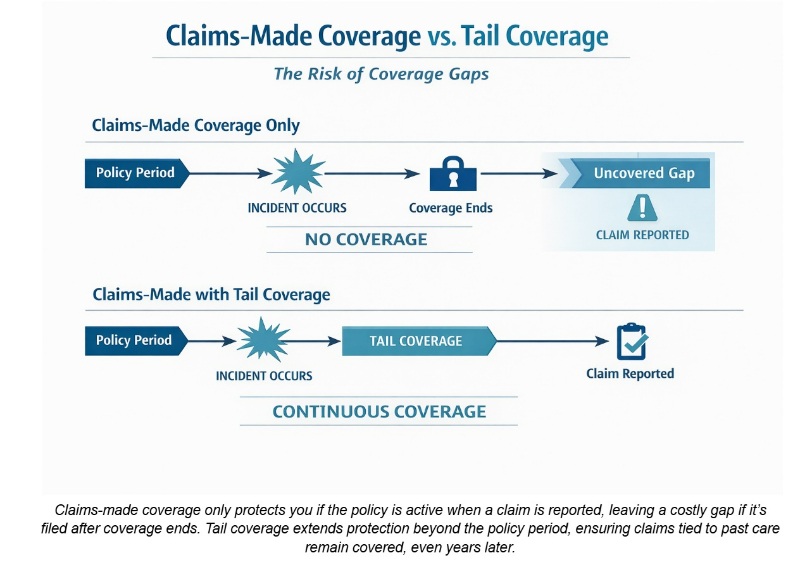

Most physicians remain insured under claims-made malpractice insurance policies, which only provide coverage if the policy is active at the time a claim is reported. According to the American College of Physicians, 97% of young physicians entering a new practice are offered malpractice insurance as an employment benefit, and nearly all of those policies are structured as claims-made coverage. While the liability landscape has changed, the insurance structure has largely remained the same.

That’s why coverage gaps aren’t minor mistakes anymore. Tail coverage is no longer a technical add-on to consider when terminating the contract. It is long-term financial protection.

Claims-Made Coverage Creates Hidden Exposure

The majority of malpractice policies in the United States are written on a claims-made basis. This structure is common and widely accepted but frequently misunderstood. A claims-made policy provides coverage only if:

- The care occurred after the policy’s retroactive date.

- The claim is made and reported while the policy is active.

If the policy ends, the coverage ends. This is where hidden exposure begins.

When a physician changes employers, retires, or closes a practice, the claims-made policy typically ends. From that moment forward, any claim tied to prior care is uninsured unless tail coverage has been secured. Many physicians assume that because they were insured when they performed the procedure, they remain protected. Under a claims-made structure, that assumption is incorrect.

This applies specifically to claims-made coverage. Under an occurrence policy, coverage is triggered by when the incident (medical care) occurred, not when the claim is reported. If the incident happened while the occurrence policy was active, coverage remains in place even if the physician later changes jobs, retires, or closes a practice. No tail coverage is required for an occurrence policy.

The structure matters. And for most physicians, it is the difference between being protected automatically and being exposed if the tail is not purchased when a claims-made policy ends. Occurrence form coverage is not available in all situations, but it is worth exploring if your practice qualifies for occurrence form coverage to avoid the future need for tail coverage.

More information here:

10 Things You Want to Know About Medical Malpractice

4 Malpractice Insurance Pitfalls to Avoid

When Coverage Ends, Liability Does Not

Misunderstanding the gap in coverage is the most common (and expensive) mistake a physician can make. The exposure is not obvious until a claim arrives years later. At that point, the opportunity to correct it is gone. Tail coverage, in most cases, needs to be purchased within 30 days of the policy expiration.

For example, a physician may leave a hospital system after several years of practice. Two or three years later, a patient alleges a delayed diagnosis tied to treatment that occurred during that earlier employment. Without tail coverage in place at termination, no insurer is obligated to defend or indemnify against the claim.

With today’s policy structures and career transitions, malpractice coverage involves more than simply renewing a policy. The broker’s role has naturally expanded into that of a risk advisor, helping doctors understand how retroactive dates, reporting windows, and employment transitions align with real-world litigation timelines.

Past Care Is Creating Long-Term Liability

Malpractice liability is often delayed. Many of the most severe claims involve injuries discovered years after the care was provided, and some specialties have longer exposure periods due to the nature of the care they provide and/or how individual state statutes of limitations are structured. For example:

- In obstetrics, claims involving minors may have extended filing windows. In some states, the clock doesn’t start until the child reaches adulthood.

- In oncology and surgery, long-tail claims are often driven by delayed diagnosis and late-emerging complications.

Most states also apply discovery rules, allowing claims to be filed within a defined period after an injury is discovered rather than when the care was provided. Tolling provisions can further extend filing timelines. In other words, liability can outlast employment and even retirement.

At the same time, third-party litigation funding has expanded significantly, lowering the financial barrier to plaintiffs pursuing complex, high-severity cases.

While the number of malpractice payments has fluctuated, average payment amounts have trended upward. This suggests a shift toward fewer but more severe claims. Fewer claims do not mean less risk; they often mean higher financial stakes per claim.

Most physicians will never face a massive, career-altering verdict. In any given year, only a small percentage of US doctors, roughly 1%-2%, have a paid malpractice claim. Still, over the course of a career, about 1 in 3 physicians can expect to be sued at least once. When high-severity cases do occur, the financial consequences can be enormous. Malpractice risk is less about how frequently you are sued and more about how costly a single claim can become.

Past care can generate liability years later. If coverage has ended without tail protection, there may be no policy available to respond.

More information here:

What Is Social Inflation, and How Does It Impact the Rising Costs of Medical Malpractice Insurance?

Umbrella Insurance and Medical Malpractice: Do They Overlap?

Nuclear Verdicts Are Increasing the Risk of Being Uninsured

Severity is now one of the defining characteristics of malpractice litigation. A nuclear verdict, commonly defined as an award exceeding $10 million, is no longer an anomaly in catastrophic injury cases. Data cited by the American Medical Association shows that in 2024, the 50 largest medical malpractice verdicts averaged $56 million, a significant increase from $32 million in 2022 and $48 million in 2023.

Birth trauma, severe neurological injury, and delayed cancer diagnosis cases frequently result in awards that far exceed traditional policy limits.

In many states:

- Non-economic damage caps have been challenged or narrowed.

- Economic damages, such as lifetime medical expenses, remain uncapped.

- Jury expectations around long-term care compensation have increased.

This creates a widening gap between standard malpractice limits and potential verdict outcomes.

Tail Coverage Reduces Uncapped Exposure

Now compare that exposure to the cost of tail coverage. Tail coverage typically costs 2-3 times the annual premium of the expiring policy. In contrast, a nuclear verdict can exceed $10 million, and a thermonuclear verdict can surpass $100 million.

When a physician declines tail coverage after terminating a claims-made policy, the decision is not a cost-saving measure. It is a decision to personally absorb uncapped exposure tied to prior years of practice.

3 Keys to Effective Tail Protection

Tail coverage, formally known as an extended reporting endorsement, allows claims to be reported after a claims-made policy has terminated. It preserves protection for prior years of care.

The three pillars of tail insurance are:

- Retroactive date: Coverage must maintain continuity with the original retroactive date to prevent gaps.

- Duration: Some endorsements provide limited reporting periods. Others provide unlimited reporting. Duration should align with specialty exposure and jurisdictional timelines.

- Policy limits: Limits should be evaluated against today’s verdict environment, not historical averages.

Tail coverage does not eliminate malpractice risk. It ensures that when past care is challenged, there is a policy in place to defend and indemnify.

When Tail Coverage Is Required, and Why These Moments Are High Risk

Tail coverage becomes necessary when a claims-made policy ends without replacement prior acts coverage.

Common trigger events include:

- Changing employers

- Selling or closing a practice

- Retirement

- Transitioning to locum tenens

- Switching specialties

These transitions are high-risk moments. Physicians focus on new roles, compensation structures, or retirement planning. The exposure, however, is backward-facing. Each prior year of practice represents potential liability. Without tail coverage, that exposure becomes uninsured immediately upon policy termination.

Specialties with extended liability horizons—including obstetrics, surgery, oncology, and emergency medicine—face particularly heightened exposure during these transitions.

More information here:

How to Survive a Medical Malpractice Lawsuit

How Physicians Can Prevent Getting Sued

Tail Coverage: Strategic Protection in a Rapidly Changing Liability Climate

Malpractice risk has intensified. Verdicts are larger. Filing timelines are longer. Discovery rules and delayed-diagnosis claims allow litigation to arise years after care was delivered.

Claims-made policies remain a standard structure in the market, but they are time-sensitive by design. When a policy ends due to a job change, practice closure, or retirement, the ability to report future claims related to prior care also ends. The exposure does not.

Tail coverage does not prevent a lawsuit. It preserves the protection already in place for past practice. Without it, years of insured care can become uninsured the moment a policy terminates.

In my experience, few decisions have a greater long-term impact on a physician’s financial security than how coverage is handled at transition. The consequences are rarely immediate. They surface later, often unexpectedly, when a claim is filed years after the care in question. By that point, the opportunity to revisit the decision is gone.

Thoughtful planning at the end of a claims-made policy is not routine paperwork. It is strategic risk management.

[FOUNDER'S NOTE BY DR. JIM DAHLE: Doctors need malpractice coverage. It is the first line of defense in any asset protection situation, and almost all of them will be involved in at least one malpractice lawsuit during their career. If their primary coverage is claims-made and not occurrence, then they need tail coverage. Period. Ideally, the employer pays for it, but if they don't, the doctor needs to buy it. The bill for that is often higher than expected. The cost of my malpractice coverage has trended down over the last 16 years since I left the military, but when I priced tail coverage back then, it was three times the annual cost of a claims-made policy. My group subsequently switched to occurrence coverage, and I would have been responsible for writing that check if I had quit my pre-partner job.

In that respect, I fully agree with the post above emphasizing the importance of tail coverage. What I do not agree with, however, is the classic fear-mongering about lawsuits that often leads doctors to lie awake at night; quit medicine earlier than they otherwise would; and embark on expensive, complicated, questionably effective asset protection journeys. When the author writes, “Most physicians will never face a massive, career-altering verdict,” believe him. It's true. While the number of above policy limits judgments not reduced on appeal is not zero, it certainly rounds there, and as near as I can tell, that risk is mostly going down, not up.

My malpractice insurance cost is dramatically less than it was 16 years ago, and Utah last year became the first state in the country that guarantees no above policy limits judgments so long as you carry at least $1 million in malpractice coverage. Hopefully, that trend catches on. Plaintiffs and their attorneys aren't really losing anything from laws like that, since those cases were so darn rare before. But it matters a lot to doctors. The bottom line is that you still need to buy appropriate malpractice coverage (including a tail), buy personal liability coverage (umbrella), max out retirement accounts, know your state asset protection laws, put rental properties in LLCs, and title properties properly. But relatively few doctors will want to go beyond that with asset protection techniques, at least until there is another business or estate planning reason for any particular technique, such as a trust or business entity.]

Do you have claims-made or occurrence malpractice insurance? Have you had to buy tail coverage in the past? How much did it cost? Was it worth it?